Latest Posts

The Power of Pausing

Lifelong Learning | 2026-05-31 04:14:37

Silence on this blog means one of two things. Either everything has stalled or too much is happening to capture in real time. For me, it has been the latter.

After wrapping up a school year traveling through Latin America, our family shifted into a completely different kind of hiatus. We returned to the States for a stationary gap year, and the pause completely changed my perspective.

The Traveling Gap Year

Looking back at our school year on the move, it was a profoundly rewarding experience for our family. It exposed us to incredible cultures and gave us memories I would not trade for anything. But it also required a lot of resilience built through trial and error.

The reality of constant travel is the sheer mental bandwidth it consumes. I generally handled daily safety and food, my wife managed lodging and routing, and together we kept the kids on track with schooling. That relentless pace left little space for quiet reflection.

It also made it difficult to build a lasting community beyond our immediate family. While we had each other, our kids deeply missed consistent, long-term connections with peers their own age.

The Home Gap Year

Our year back home was shaped by a new script. I wanted to see what life could look like outside of a traditional career path, explore my interests in real estate and personal finance writing, and spend intentional time with family and close friends. Meanwhile, my wife took on a full-time public school teaching job for the first time in her career.

I wanted to be fully present. Working in education meant my attention had always been divided between my own kids and the school community. Being home shifted my focus entirely to my family, and it has been a true gift.

Staying put meant I could show up for everything:

*The daily milestones: Track meets, cybersecurity club, band performances, and parades.

*The cultural rhythm: Helping my daughter navigate her first experience in an American public school, while supporting my son through the increased academic demands of a heavier homework load.

*The quiet evenings: Instead of spending nights planning for the next school day, I could sit with my kids, ask about their day, and talk about their hopes and dreams.

Living in one place definitely came with tradeoffs. While the kids loved being near family and a steady routine, they really missed the conversational, inquiry-based style of their international school. Instead, they bumped up against a public school setup that feels a lot more focused on standardized testing. It can be a bit rigid, which sometimes leaves less room for just following a spark of curiosity. They’ve also felt the absence of their former global peers. In their old schools, different backgrounds naturally sparked lively debates. Here, American teenage social pressure seems to make kids a lot more hesitant to speak up. It often leaves my kids awkwardly realizing they are the one of the few students answering the teacher's questions.

The Big Breakthroughs

For years I lived in Europe and watched the Financial Independence (FI) community grow from afar. Working on an educator schedule made it difficult to plug in, so becoming an active part of it this year has been especially rewarding. I have met regularly with local groups and even led a discussion on worldschooling at a regional meetup.

Having the space for reflection also challenged my sense of identity in unexpected ways. I spent years asking students to wrestle with who they are without fully engaging those questions myself. Clarity came through long morning walks, extra workouts, and still moments at home. In that space, I realized I want to serve others more broadly while still protecting time for family.

At the same time, putting down roots forced me to move past theory and confront the messy reality of my business ideas.

I managed the replacement of 80-year-old pipes in our occupied local fourplex. It was a literal trial by fire. Navigating plumbing failures alongside tenant logistics grounded me in the day-to-day reality of property ownership. It also gave me pause about scaling. Seeing markets like Tennessee skyrocket made me realize the investment window is narrowing, and out-of-state landlording might not fit the life I actually want to live right now.

I also began writing about personal finance (as you are reading here) on my own terms, focusing on depth rather than chasing a larger following.

Unretiring

Testing the waters of a work-free life taught me an unexpected lesson. While I appreciate the autonomy it brings, I am not ready to step away from education permanently.

The quiet months did not dull my passion for school leadership. Instead, the time away cleared out the professional fatigue I felt, leaving the core of what I love fully intact.

I missed the energy of the international school environment, but I also knew I needed an adventure that matched a newfound commitment to personal balance.

A few months ago, the right opportunity emerged, and I accepted a new administration role at a smaller international school in Africa. This decision reflects a shift in how I view my career, shaped by an idea from “The Simple Path to Wealth” by JL Collins. In the FI world, building a financial runway is ultimately about buying back your options.

For me, that financial stability means I can step into this new role focusing entirely on the school's mission rather than my own career advancement. It allows me to lead with honesty and directness, putting my energy into building a culture where people genuinely grow. I step into this role with a lighter heart and a clearer mind.

Moving Forward with Intention

As I prepare to return to international school administration, I am carrying forward a renewed commitment to healthy boundaries.

Taking two gap years, first traveling and then living a stationary life, permanently shifted my perspective. My kids are much closer to adulthood than childhood, and these months at home taught me the importance of keeping my energy balanced. In the past, it was easy to let the demands of running a school consume every evening and weekend. Moving forward, I want to ensure my family gets the best of my energy, not just what is left at the end of the day.

This mindset will directly shape how I lead. The culture of education often praises long hours, but a depleted leadership team ultimately cannot serve students at the highest level. By managing my own time with greater efficiency and focus, I hope to model a healthier approach for my staff, proving it is entirely possible to care deeply about the school's mission while maintaining a balanced life outside of it.

Discovering Index Investing

Index Investing | 2025-11-14 16:58:28

A Note Before We Begin

As always, I need to start by reminding you that I am not a financial advisor and this is not financial advice. This is simply my personal story of how I got started with index investing and what I have learned so far. Everyone’s financial situation is different and investing involves risk. You could lose money, so if you are inspired to take action, do your own research and consider consulting a certified financial advisor.

How I First Heard About Index Investing

I first learned about index investing while working overseas in an international school. One of my colleagues, a mid-career professional who had transitioned from finance to teaching design classes, shared how he managed his investments. Rather than picking individual stocks, he invested in index funds that tracked large sections of the market including small, mid, and large caps, international markets, emerging economies, and bonds. He even shared the percentages he allocated to each fund. I was fascinated by how simple and inexpensive his approach seemed. Hearing him talk made me realize there was a way to participate in the market without constantly guessing which stock would win.

What Index Investing Actually Means

Index investing is based on a simple idea. Rather than trying to pick the next winning stock, you buy a fund that owns many of them, often all the companies in a given market index. An index might represent large U.S. companies, the entire U.S. stock market, or a specific region of the world. The goal is not to outsmart the market but to match its performance.

Because there are no expensive fund managers selecting individual stocks, index funds tend to have low fees. Over time, this often leads to better results than most actively managed funds. Index investing also provides diversification, simplicity, and peace of mind.

Early Constraints and Learning

At that stage, we had been largely a single-income household of four, so I had not had much extra cash to invest outside of real estate, which I mostly funded with debt. Later, a high school economics teacher at my school expressed a similar philosophy about buying the market instead of trying to beat it, echoing the approach of the design teacher, and the idea stuck.

I began reading books like The Millionaire Teacher and The Millionaire Expat by Andrew Hallam, himself a former international school teacher. I also explored The Simple Path to Wealth by JL Collins, The Millionaire Next Door by Stanley and Danko, and The Psychology of Money by Morgan Housel. These books stood out for their clarity, simplicity, and optimism. They helped me understand that investing did not have to be complicated. I just needed to build steady habits and stay consistent over time. At some point I will write reviews for each of these books.

Index Funds Versus ETFs

When I began, I used traditional index mutual funds, which you buy directly from companies like Vanguard or Fidelity. These funds are priced once per day after the market closes and make it easy to set up automatic contributions. Later, I discovered ETFs, or exchange-traded funds, which track the same indexes but trade like stocks throughout the day.

ETFs are often slightly cheaper and more tax-efficient, and they can be bought or sold anytime during market hours. Traditional index mutual funds, on the other hand, are convenient for automation and regular investing. Both options provide broad, low-cost exposure to the markets, so the choice usually depends on whether you prioritize automation or intraday trading flexibility. Keep in mind that costs, tax benefits, and automation options can vary depending on the specific fund and the platform you use to invest.

Market Crashes and Lessons in Emotion

I began investing during the 2018 stock market drop, which prompted me to open my first brokerage account. Stocks felt like they were on sale and even though I did not know much at the time, I realized it was a good moment to start. From there, I contributed regularly using dollar-cost averaging. This means investing a fixed amount at regular intervals, whether the market is up or down. It removes emotion from the process and ensures you buy more shares when prices are low and fewer when prices are high. Looking back, this experience taught me that discipline matters more than timing the market.

A couple of years later, the COVID-19 market crash arrived in early 2020. Stocks fell sharply and this was the first time I experienced a market downturn while actively invested. It showed me what it really looks like when the market goes on sale and taught me how to maintain that mindset even as the value of my own investments dropped. I jumped in aggressively, buying more than ever and taking full advantage of the discounted prices. I remember the mix of excitement and anxiety as I watched prices swing wildly. That period reinforced how valuable it is to have a plan.

Like many new investors, I tried a few individual stocks and quickly realized how much effort it took to analyze each company and predict its performance. The constant decisions and second guessing showed me that focusing on individual stocks was not for me. Index investing made more sense. I could participate in the growth of the entire market without trying to pick winners or losers. I only needed to stay patient and let time do the work.

How My Portfolio Evolved

I started by following my colleague's suggestion of directly controlling the weighting of small, mid, large, foreign, and emerging stock indexes and bonds. Over time, my portfolio evolved to about sixty percent in a total U.S. market weighted ETF, twenty percent in international markets, and twenty percent in bonds. This advice came from a fee-only investment adviser. More recently, I have added a tilt toward small-cap and value funds and reduced the bond exposure.

These adjustments reflected my growing confidence in long-term stock investing and my appreciation for the efficiency of ETFs while also adding some risk to balance my relatively low-risk real estate holdings.

I still miss how easily I could automate contributions with traditional index mutual funds, but ETFs have given me liquidity and tax advantages. While living overseas, taxes were minimal thanks to the foreign income exclusion. Now, back in the United States with some family W-2 income, I see how quickly taxes can eat into profits if a portfolio is not managed carefully. I have become more strategic about where I hold dividend stocks and bonds, and I pay closer attention to tax efficiency when making investment decisions.

Final Thoughts

What I appreciate most about indexing is its calm simplicity. You do not need to outthink the market or constantly check stock prices. You just need to participate in the growth of the economy as a whole. My message to anyone new to investing is simple: start small, stay diversified, and let time, not emotion, be your greatest ally. Reflecting on my journey, I see that even small, consistent steps can lead to meaningful results and that confidence grows as knowledge and experience accumulate.

Harvest Season Living Lightly on Taxes This Year

Lifelong Learning | 2025-11-05 11:14:56

Intentional Tax Planning

This year I am taking a broader, more intentional approach to our taxes. I want to manage all types of income including wages, passive income, and investments so that total taxes stay reasonable while remaining fair and sustainable.

I am harvesting long-term capital gains and dividends. This means selling investments at a gain to take advantage of favorable tax rates. I am also using Roth conversions strategically, moving money from a traditional IRA to a Roth IRA. This allows me to pay tax now while letting future growth remain tax-free. Timing is important and these steps work together as part of a larger plan.

I am inspired by Vicki Robin, author of Your Money or Your Life. Her work emphasizes aligning money with values and showing how financial decisions can reflect the life you want rather than simply chasing dollars.

Perspective and Background

This year is part of our mini-FI experiment, focused on living off investment and passive income instead of full-time work. Early in my career, I handed my accountant a shoebox of receipts and relied on him to sort everything out. Nearly two decades later, I married my wife, a former economics and accounting major, who guided our taxes for many years. Now I manage most of it myself and am learning firsthand how different types of income are taxed.

Experts have shaped my thinking along the way. Mr. Money Mustache, a personal finance blogger, advocates conscious spending, early retirement, and proactive financial planning. Ben Carlson, investment strategist and author of A Wealth of Common Sense, offers insight into tax-efficient investing and income management. I also plan to read Tax Planning to and Through Early Retirement by Cody Garrett and Sean Mullaney this next year to deepen my understanding of these ideas.

Ethical and Legal Context

This reflection describes my personal approach rather than professional advice. Strategies such as gain harvesting, Roth conversions, and timing income are complex and may not be suitable for everyone. I expect to make mistakes and am prepared to pay any extra taxes or fees as part of the learning process. Anyone who wants to avoid this complexity should consult a qualified tax or financial professional. My goal is to manage taxes responsibly while contributing fairly to the broader community.

While these strategies are legal when followed correctly, mistakes in timing, calculations, or account rules could result in penalties or unexpected taxes. Ethically, using timing or exclusions to minimize taxes can raise questions of fairness even when done responsibly. I aim to balance personal financial planning with contributing fairly to society, acknowledging that some choices like using the foreign income exclusion or harvesting gains strategically have both legal and ethical nuances. Being mindful of these complexities helps me approach taxes thoughtfully while supporting both our family goals and the broader community.

Tax-Gain Harvesting and Timing

By November my income picture is clear enough to start fine-tuning taxes. Acting early allows me to make adjustments instead of waiting until April when the numbers are already set. I am harvesting long-term capital gains from my brokerage account while aiming to stay within the 0 percent capital gains bracket. In 2025 this applies to taxable income up to $96,700 for those filing jointly. To figure out how much I can safely harvest, I project total income, subtract the standard deduction of $31,500 for married filing jointly, and estimate how much gain can be realized before moving into the next bracket. These thresholds change periodically so it is important to check current figures before planning.

I treat this brokerage account as a flexible alternative to a 529 plan. It can fund education abroad, starting a business, or more traditional learning opportunities in the United States if my kids choose. It also serves as my early retirement fund. To prepare for tax season, I turned off automatic dividend reinvestment in all accounts holding the funds I plan to sell.

I recently made a mistake when I bought and quickly sold a fund. While I am not trying to harvest a loss, the IRS wash-sale rule would disallow the loss if I repurchased the same security within 31 days. It would also adjust the purchase price of the new shares, complicating future gains or losses. Because of this, I am now waiting the full 31 days before making similar trades. At the same time, I am using a small Roth conversion to raise taxable income enough to capture the full child tax credit. This allows the funds to grow tax-free over time.

Fairness and Overall Tax Rate

Taxes can sometimes feel unfair. When we lived overseas, we benefited from the U.S. foreign income exclusion and did not pay Polish taxes due to tax treaties. This sometimes seemed unfair to the locals we worked with. We drove their roads and enjoyed their parks while contributing our professional skills but not fully contributing to their public system.

Back in the United States, we paid no income or Social Security taxes during our years overseas, which will reduce future benefits. However, we did pay substantial property taxes in Washington state, roughly 40 percent of the net income from our real estate business. Real estate taxes can be complex. Depreciation lowers taxable income on paper, but those savings eventually go toward repairs, roofs, and maintenance. Focusing on actual taxes and costs paid provides a clearer picture of the real cost of earning income through real estate.

Keeping our effective tax rate around 20 percent across all sources of income feels like tending our financial garden responsibly. Much public debate focuses on W-2 taxes largely paid by the middle class while often overlooking stock options, capital gains, and other income sources more common among the wealthy. When we have control over our income streams, it is important to use that control wisely and responsibly.

Final Thoughts

This year’s approach to taxes has been an exercise in intentional planning. By managing them thoughtfully, I can shape how our income and investments support the life we want to lead. The experiment in tax-gain harvesting and Roth conversions has reinforced how much control we actually have over our tax picture.

When our effective tax rate ends up below our target, we plan to increase our giving through charitable donations or community support, returning to the systems that make our opportunities possible. In this way, taxes and giving become more than obligations. They are a way to live intentionally and responsibly, supporting both our personal goals and the broader community. I will check back in a few months to share how this approach played out once our taxes are fully processed.

Minimalism Beyond Things

Minimalism | 2025-10-21 15:47:17

This is part two of a four-part series on minimalism. Feel free to scroll down to read my previous reflections on my early journeys with minimalism and managing physical possessions.

Expanding My Minimalism Mindset

Simplifying possessions showed me how liberating minimalism can be. Over time, that mindset extended beyond clutter into how I spend time, manage attention, and make choices in how I spend money. Minimalism is not just about owning less. It is about living with purpose. Before, my days often felt like a race against time, filled with tasks, noise, and commitments. Simplifying has given me more mental space, less stress, and greater freedom to focus on family, friends, creative projects, and reflection.

Simplifying Time, Commitments, and Routines

Minimalism has taught me to simplify not only what I own but also how I use my time. Taking on too much socially or professionally leaves little room for anything else. As a teacher, I learned this the hard way. I once taught a full load while directing extra-curricular choirs before and after school. Another year, I coached football and once the season was completed I produced a musical at my school. Over time, I learned to take on only one extra commitment at a time and to take a break between demanding projects. Socially, I now prioritize family and maintain a smaller, intentional circle of friends to leave space for genuine connection.

I experiment with routines, from weekly meal planning to setting aside mornings for deep work and afternoons for lighter tasks. Balancing creativity and structure is not always easy because spontaneity can conflict with the plan. These small choices, however, free mental space and make life calmer. Choosing experiences over possessions has reshaped how I see value. Moments spent sharing a meal with friends or walking with family last far longer than any new gadget or outfit.

Digital Decluttering

Digital clutter can be as draining as physical clutter. I have reduced email subscriptions, deleted distracting apps, limited social media, blocked unknown callers, and bookmarked key websites. Habits like silencing notifications and keeping my phone in another room while I sleep help me stay present. Limiting screen time and breaking up long computer sessions with outdoor activity, movement, or time with family and friends increases the joy in my life.

Financial Freedom and Mindful Spending

Minimalism is closely tied to financial freedom. Distinguishing needs from wants and avoiding impulse purchases allows me to save for what brings lasting value, from experiences to investments. I once bought a used truck for ten thousand dollars and later sold it for five. If I had spent only five thousand and invested the rest in the S&P 500, that money would have grown to about thirty-seven thousand dollars today. Small financial choices can add up, you just have to decide what brings the most value to you.

When we recently moved back to the United States, we furnished our home for a few hundred dollars using various sources, with Facebook groups particularly helpful, focusing only on what we truly needed. When moving from other homes, we downsized by selling or giving away possessions. The greatest joys were the positive energy that came from these simple, generous interactions.

Acknowledging Other Perspectives

While minimalism has helped me find balance and clarity, it is not the only path. Some people thrive on full calendars or find comfort in spaces filled with memories. For others, simplifying can feel limiting rather than freeing. What matters most is that our choices, minimalist or not, reflect what we value and what brings meaning. Minimalism just happens to be the path that works for me.

Enhanced Freedom and Creativity

Less clutter, fewer distractions, and simpler routines create space for creativity. Whether in music, teaching, writing, or personal projects, minimalism helps me approach work with clarity and focus. Fulfillment comes not from having more but from appreciating enough. Minimalism does not take away. It gives space to live intentionally, honor values, and create a balanced, meaningful life.

Minimalism | 2025-10-17 18:12:17

Finding Freedom in Less: How My Journey Began

Minimalism | 2025-10-17 17:17:55

What Minimalism Means to Me

Minimalism to me is more than decluttering or getting rid of stuff. It is a way of living intentionally, removing distractions, and creating space for what truly matters. It is about a life of purpose, focus, and meaning. I have come to see minimalism not as a destination but as a journey that unfolds over years of reflection, experimentation, and small deliberate choices.

Over time I have simplified my possessions, pared down my wardrobe, and learned to recognize the items and commitments that genuinely enrich my life. Minimalism is not about perfection. It is about noticing what weighs you down, choosing what is important, and moving aside what no longer serves you. This process evolves as life and circumstances change.

Early Challenges with Clutter

I first realized the need to downsize in 2005 when I moved to China. My garage was overflowing and as a choir teacher I had classrooms at two schools along with an extra room at home all filled with belongings. I remember selling or donating most of my possessions and keeping only one storage room with shelves and a motorcycle. Gone was my truck, much of my wardrobe, and many decorative items, though I still kept some memories boxed up for another day.

This experience made me question the endless accumulation of things I had gathered over time. I thought about decorative objects that once seemed meaningful, the extra clothes I rarely wore, and the small dolphin figurines collected from childhood into adulthood. I began to see the difference between what I thought I needed and what was truly useful. That insight deepened when I noticed a friend living contentedly with only enough clothes for a single week.

The cycle repeated after I married, moved back to the United States, and started a family. Much of the clutter built up during those years, but I still held on to older possessions from previous moves, my time in China, and even my youth. My son had also begun to collect and keep things much as I once had. I wanted to model a simpler way of living for him without forcing it on him, showing that clearing away the unnecessary can create space for what truly matters. Each round of sorting reminded me how easy it is to accumulate and how light life can feel when excess is removed.

Turning Points

Some of the most transformative lessons came from the practical constraints of moving. When we moved to Poland, we traveled with only one large suitcase and one small suitcase each, living with just what we could carry and adding only what was essential as we settled in. Those years showed us how much clarity and ease come from simplicity. Later, during a year of world travel without a permanent home, we experienced that clarity again. For a year, the four of us carried only a small backpack each, including a laptop and just enough clothes for a few days at a time. Each move reminded us how much more space there is for meaningful experiences when possessions are limited.

Another turning point came when I began simplifying routines. Professionally I reached a point where I could plan what I would wear for the entire workweek on Sunday evenings, keeping only enough work outfits for six days, much like the friend I had once admired. Streamlining wardrobe, meals, and holiday plans brought unexpected peace. These small shifts guided by a minimalist mindset helped me focus less on managing things and more on living with clarity and purpose.

Ongoing Process

Even now, minimalism is a work in progress. Recently, I counted my personal memory boxes, which include school yearbooks from middle school through college and most of my teaching years, mementos from my time as a stage actor and singer, awards and other teaching memories, childhood toys, my letterman jacket, and even my high school show choir sequin vests believe it or not. I have them down to just eight boxes. My sheet music collection, which I admittedly tend to hoard and which has its own file cabinet, is another ongoing project. It includes pieces with sentimental value, such as my grandparents’ organ music, compositions I have written, and nearly every choral song I have ever performed or taught. I have already reduced half a box and plan to continue thinning it in the coming months, keeping only the pieces I am likely to use again.

Each summer, I spent time opening one of my memory boxes, sorting through its contents, and deciding what I was ready to release and what I wanted to preserve. This practice is how I managed to get the collection down to eight boxes, even though they became fuller again after moving back from Poland. Now that I am back home in the United States, I dedicate regular time every few months to maintaining this habit.

Lessons Learned

Throughout this journey, I have learned the difference between needs and wants, the value of intentionality, and the power of clearing away what is unnecessary. Minimalism is not just about making space for things. It is about creating mental clarity and opening room for meaningful experiences. It encourages you to question purchases, routines, and commitments, helping you align your life with your values.

I have discovered that with minimalism, you can fully furnish a home for just a few hundred dollars, prioritize experiences over possessions, and find joy in simplicity. It is not about deprivation. It is about focus, lightness, and the ability to live life on your own terms.

Closing Reflection

Minimalism is a continuous journey of reflection, intentionality, and growth. While I still have possessions to pare down and routines to simplify, every step I take reinforces the value of focusing on what truly matters, both materially and spiritually. My story shows that even small, deliberate choices can transform a life weighed down by excess into one filled with clarity, purpose, and ease.

Tennessee Road Trip and Lessons Learned

Real Estate | 2025-10-10 18:04:19

Arrival in Nashville

We landed in Nashville to a city buzzing with live country music, glowing downtown lights, and that Southern warmth that makes every stranger feel like a friend. A new stadium rising nearby hinted at a city on the move. Since our flight had arrived late, we checked into the hotel and called it a night, saving our energy for the road ahead.

Hitting the Road in a Convertible

The next morning, adventure arrived in the form of a convertible Mazda Miata. It looked ready for a joyride with the top down, but Tennessee humidity had other plans. With the top sealed tight and the air conditioning working overtime, we set off through rolling green hills and thick forests. Every so often, the trees opened to reveal a small-town main street, a whiskey distillery, or, most often, the glow of a Waffle House sign. Driving was an adventure in itself as my friend, whom I believe missed his calling as a stunt driver, handled the curves and chaos with ease. We saw a few close calls from erratic drivers and noticed a curious local habit where people in the slow lane would drift into the fast lane right in front of us, then creep past the car they were overtaking.

A BBQ Stop to Remember

Our destination was a small community outside Chattanooga, where we had a walk-through scheduled for a four-unit property. But first came barbecue. We were about to stop at a burger joint when smoke rising from a nearby food truck changed our plans. The smell alone was enough to reel us in. I ordered a beef brisket sandwich, something I rarely eat, but it turned out to be an unforgettable meal. The tender, smoky meat practically melted in my mouth.

First Impressions of the Property

The four-plex sat in a quiet neighborhood of tidy brick homes that gave the area a warm, family feel. From a distance, the property looked promising but up close it told another story. The driveway and walkways were cracked and uneven, and the neighboring lot sloped toward the house, suggesting drainage issues. We could even trace the path of water runoff during heavy rains. The porch supports were worn or missing and a large tree grew too close to the foundation, where we saw cracking. The brick siding and trim showed wear, and the roof was dotted with loose shingles and debris. From the listing photos, we had already noticed the lack of gutters, common in snowy regions but puzzling in Tennessee’s rainy climate.

Inside and Under the Home

At first, I thought the exterior issues could be manageable with time and effort. But once we stepped inside, the tune changed quickly. Moisture appeared to be the main problem, immediately noticeable in the heavy, damp air that met us at the door. The first apartment smelled musty, and we could feel the humidity clinging to the walls. The crawl space told the rest of the story as we saw standing water, patches that looked like fungus, and dark streaks along the joists. Inside the units, floors were uneven, walls were cracked, and ceilings showed stains that suggested long-term leaks. Several windows and doors stuck or would not close properly, and a few fixtures needed attention. The electrical setup appeared questionable, with panels located in odd places and outlets missing modern safety protection. Plumbing looked dated as well, with older pipes and some improvised wiring near the water heater. The property seemed to need professional attention across several areas, including structural, electrical, and plumbing systems. While I am not afraid of a project, this one looked gigantic and unlikely to yield a profit for quite some time after a major investment. I also found myself thinking about the tenants already living there and the potential health and safety implications of prolonged moisture issues. In the end, we decided against moving forward on the property.

Lessons Learned

On the drive back, I realized that Chattanooga is too far from the Nashville airport. The long drive added unnecessary complexity and made the logistics of any future work difficult. If we want convenience and efficiency, our next target needs to be a property within thirty minutes of an airport that offers a single-flight connection from Seattle. No more long drives after arriving or before departing. We also left with a new appreciation for the power of pre-screening before ever setting foot on a property. Doing your homework can save hours of travel and a lot of money. Before scheduling a walk-through, it helps to review online listings for price history, rent comparisons, square footage, and photos that might reveal damage. Google Maps can provide clues about roof condition, drainage risks, lot slope, and nearby nuisances. Public records can show ownership history, tax changes, flood zones, and permits.

Key Red Flags

>Roof, siding, or exterior showing visible damage or wear

>Poor drainage or missing gutters, especially where water runoff could affect the foundation

>Trees or branches too close to the house

>Signs of moisture, mold, or fungus in crawl spaces or interiors

>Uneven floors, cracked walls, or stained ceilings

>Outdated or potentially unsafe electrical or plumbing systems

Only after a property clears these checks should it earn an in-person visit.

Choo Choo Tracks to Tennessee

Real Estate | 2025-10-06 15:49:40

I never expected decades of investing in Washington State would lead me to Hixson, Tennessee, a northern suburb of Chattanooga. There I stood on a quiet street, looking at a weathered four-plex with a friend and potential business partner. Chattanooga had been on my mind for its affordable homes, steady population growth, and reputation as a place where landlords can still make things work. As we drove through the neighborhood, the old tune Chattanooga Choo Choo kept playing in my head, a reminder that life often takes unexpected turns.

My path to that moment began years earlier. As a young teacher, I bought my first multi-unit property in Tacoma, Seattle’s blue-collar neighbor. I lived in one unit and rented out the others to help cover the mortgage, taxes, insurance, and upkeep, which made it just barely possible to own in a desirable neighborhood on a teacher’s salary. Most teachers I knew couldn’t afford to buy nearby unless their household had a second, higher income. Today, I’d recognize that strategy from YouTube channels and personal finance books as house hacking, though I’d never heard the term back in 2000. I can thank my dad for helping me see the value in that kind of setup; he showed me how real estate could offer a bit of stability and independence. Growing up in a family that owned and managed rentals gave me the confidence to try, though I learned plenty the hard way too.

Over time, I added a few small houses and began to understand the quiet power of earning both income and equity through rentals. I kept my portfolio small enough to manage without losing focus on teaching, first at home and later overseas. A healthy and sometimes overly cautious fear of debt also helped me steer clear of trouble during the more volatile years. Teaching shaped how I see the world and deepened my appreciation for stability, community, service, and thoughtful long-term planning. Music, too, left its mark, which may be why Chattanooga Choo Choo stayed in my head as I explored the area.

Living abroad reshaped my view of risk. In some countries, homes could be bought for a fraction of U.S. prices and rented for strong returns, yet I also saw how quickly stability could disappear. A friend in Ukraine had to abandon his business almost overnight, and my family’s volunteer work in refugee centers in Poland made those lessons personal. Back in Washington, my Puget Sound properties still provide steady income, but prices have outpaced rents, property taxes continue to rise, and new regulations make expansion less appealing. More and more, the market feels tilted toward big investors with deep pockets and political connections, leaving smaller landlords like me squeezed out. That reality pushed me to look for places where the numbers still work and the environment is friendlier to individual investors.

That search brought me to Tennessee. Standing in front of the four-plex in Hixson, I thought about the choices and experiences that had led me there, from my first house hack as a young teacher to wandering foreign streets and imagining new possibilities. For me, real estate has never been just about numbers. It’s about providing safe, affordable homes and building genuine relationships with tenants, even as I figure out how to maintain those connections from afar through property managers. At its heart, it’s about freedom, security, and the belief that thoughtful choices today can open doors tomorrow. In my next post, I’ll share what I discovered in Chattanooga and whether this Southern city might become the next chapter in my investing story.

Our Year as a Nomadic Family in Latin America

Global Citizenship | 2025-10-01 22:44:22

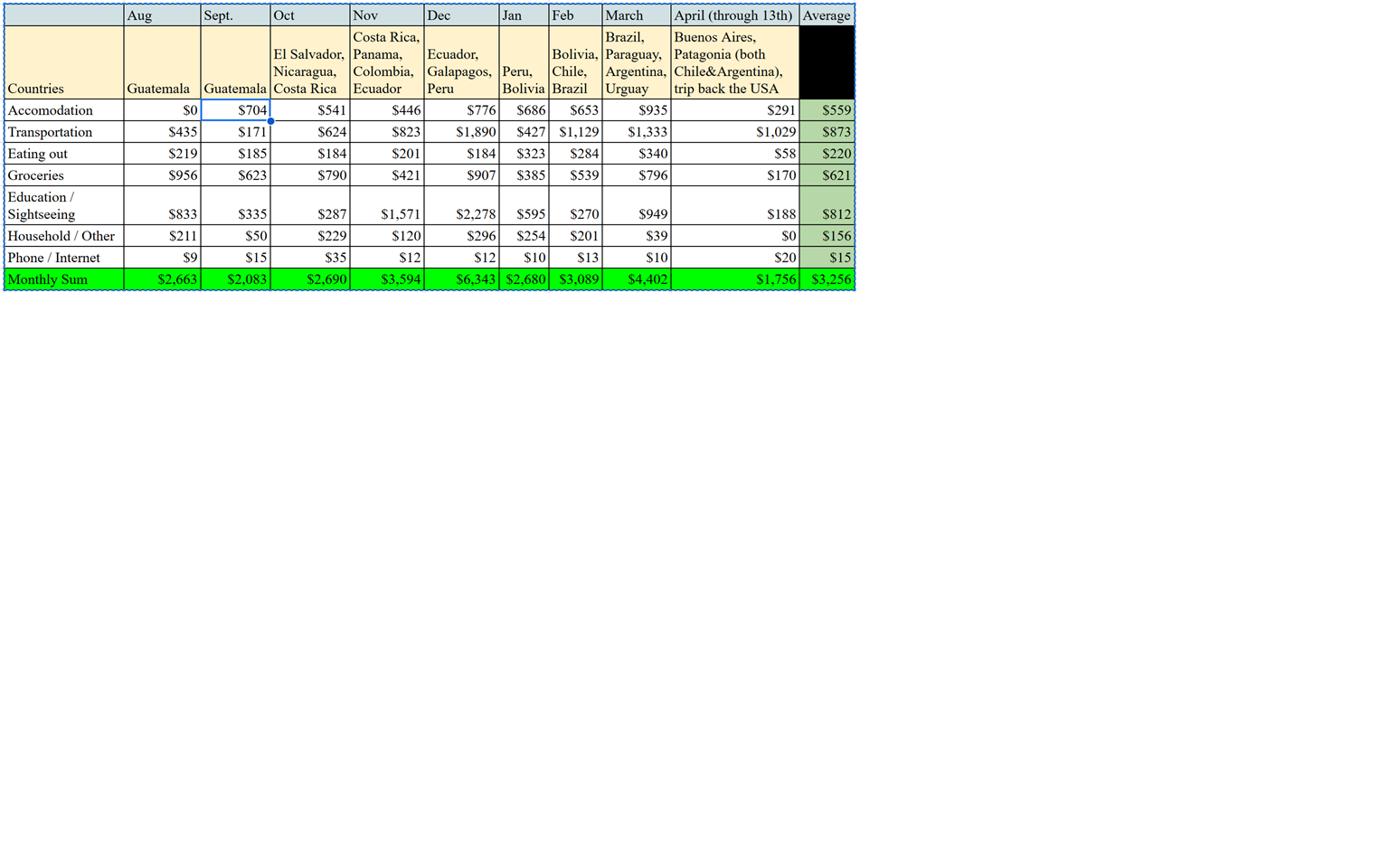

For one year, our family traded our apartment in Warsaw, Poland, for backpacks and the unpredictability of life on the road. We traveled through fourteen countries in Latin America, from Guatemala to Patagonia, immersing ourselves in local cultures. This was more than a vacation. It was, in its own way, an experiment in long-term family travel that tested our stamina, curiosity, and assumptions about money. How much does it really cost to live on the road for a year? What trade-offs make sense, and where is it worth splurging? After nine months of detailed tracking, we found lessons that went far beyond numbers, reshaping how we think about travel, family life, and what it means to invest in experiences.

Setting Out

When we began, we had only a rough idea of what a year on the road might cost, and the daily realities quickly challenged our assumptions. Would long-term travel be cheaper than maintaining a home in one place? How would flights, tours, and life’s unpredictability affect our budget? Our years in Warsaw, along with travel across Europe, the northern Middle East, and Africa, gave us context, and comparing those experiences with our time in the U.S. offered further perspective. We soon discovered that family travel can be more affordable than staying put, though expenses rose and fell with our choices and timing. Flexibility proved essential, letting us balance modest stretches with occasional splurges and see the trade-offs between comfort, adventure, and cost.

The Numbers Behind the Story

On average, our family spent $3,256 per month while traveling. Monthly totals ranged from $2,083 in September, when house-sits in Guatemala kept costs low, to $6,343 in December during our adventures in the Galápagos and Peru. Over a little more than nine months, our total came to $29,300. At that pace, a full year would have been roughly $42,000. That’s less than a typical middle-class lifestyle in Tacoma, Washington, and close to what we once spent in Warsaw, though inflation has affected both places. By keeping our fixed costs back home to a minimum, such as using storage for our possessions and not maintaining a primary residence with rent or a mortgage, long-term travel felt far more manageable. Even our occasional splurges stayed on track as long as we balanced them with steadier stretches.

Where the Money Went - Accommodations

Accommodations were far lower than we expected. By mixing Airbnbs, guesthouses, house-sits, and credit card points, we averaged $25 to $35 per night. House-sits in Guatemala, Costa Rica, and Chile nearly eliminated lodging costs at times, while points covered stays in Nicaragua, Lima, Santiago, and Uruguay. Flexibility through longer stays, off-peak timing, and creative use of points was essential to keeping expenses manageable.

Where the Money Went - Transportation

Transportation proved the most unpredictable. Local buses kept some months as low as $170, while flights and ferries to the Galápagos pushed costs up to $1,900. Renting cars was sometimes more convenient and even cheaper than taking tourist buses. Chicken Buses ranked among our favorite experiences. Deciding when to fly versus traveling overland made a significant difference, and we tried to limit flights whenever possible, mindful of their environmental impact.

Where the Money Went - Food

Food costs were moderate and allowed us to eat well. Groceries ranged from $500 to nearly $1,000 per month, with eating out adding another $200 to $350. We cooked at home during house-sits or in Airbnbs with kitchens, while local markets offered affordable, authentic meals, including freshly prepared dishes we could eat on the spot once our stomachs adapted to local food. We learned to be mindful about how food was prepared, choosing trusted vendors and freshly cooked dishes to avoid getting sick. In places like Bolivia, Nicaragua, and Guatemala, eating out was sometimes even cheaper than cooking. Even in pricier regions such as Chile, Uruguay, and Costa Rica, food costs remained below typical U.S. levels.

Where the Money Went - Education

Education and experiences were our largest investment. Multi-day eco-tours, museums, scuba diving, surfing, Machu Picchu, and snorkeling in the Galápagos became the highlights of our travels. Both kids were also enrolled in some online courses, though we found a free option for our middle schooler. We averaged about $800 per month, with splurges as high as $2,200. For us, experiences outweighed possessions, both on the road and back home.

Where the Money Went - Other

Miscellaneous costs such as laundry, visas, clothing, and SIM cards were minor, usually $50 to $200 per month. Keeping routines simple helped keep these in check.

Patterns and Takeaways

Most important, we found that spending on experiences mattered far more than cutting every logistical cost. Even in our most expensive months, traveling still cost less than running a typical household in Western Washington. Averaging around $3,200 per month allowed us to live well, explore deeply, and invest in learning opportunities for our children without ever exceeding what we might have spent at home. Now that we are back in the U.S.A., our rent and utilities alone are about the same, which makes the contrast with life on the road feel even more striking.

A year on the road revealed some clear patterns. Country choice shaped our budget, with Bolivia and Guatemala offering relative bargains, while the Galápagos, Uruguay, Chile, and Brazil, especially during Carnival, pushed expenses higher. Flexibility became essential, as last-minute house-sits or off-peak rentals often made the difference between stretching our budget and splurging. Traveling while young, healthy, and with children still at home felt like both a privilege and a wise investment. By the end of the year, we realized that the value of travel was not only in the places visited but in the shared experiences, lessons, and resilience it built as a family.

Pathways to Travel for Families

Our year on the road showed us that long-term family travel is possible without extreme wealth or waiting until retirement. A few strategies made the difference:

>Slow down. Longer stays reduced costs and stress while giving us time to connect more deeply with each place.

>Get creative with housing. House-sits, guesthouses, and off-peak rentals made lodging far more affordable than we expected.

>Use credit points strategically. Credit card and airline miles covered entire stretches of accommodations and flights.

>Spend where it matters. We prioritized experiences like the Galápagos or Machu Picchu over comfort upgrades or unnecessary extras.

>Track spending closely. Knowing where the money went kept surprises at bay and let us plan ahead for splurges.

>Create a sense of stability. Mimicking a steady income made the year feel sustainable.

As an educator with over twenty-five years of experience accustomed to monthly paychecks, I built a CD ladder to replicate a regular income stream. While it was not the highest-return option, it gave us the peace of mind to focus on family and travel rather than worrying about a dwindling savings account.

Embracing Privileges and Responsibilities: From Stability to Entrepreneurial Freedom

Lifelong Learning | 2025-10-01 20:57:47

What would it be like to step away from a predictable life and spend time exploring one guided entirely by your own choices? For many years, a steady career in teaching and school administration provided me with financial security and a reliable vantage point from which to observe the ups and downs of the U.S. economy. I am grateful for the students, families, and colleagues who shaped me as an educator and gave me the foundation to explore this new season.

That question became real during the 2024–25 school year, a season of travel and reflection with my family. While living for a month on the shores of Lake Atitlan in San Juan, Guatemala, we read and discussed Rich Dad, Poor Dad. Watching the Canadian family who ran our hotel sustain themselves while building deep ties to the local community revealed a way of life rooted in purpose and self-direction. Experiences like this, along with books such as Die with Zero, encouraged me to explore entrepreneurship and investing as possible ways to align my work more closely with my values. Stepping away from a predictable career has given me space to imagine new paths toward freedom, financial independence, and a legacy of resilience for my children.

Like my time in school leadership, I continue to structure my days with intention. Mornings are devoted to high-impact creative work, while afternoons and evenings focus on family, health, learning, and reflection. Each night I review the day’s goals and plan the next. Small wins, like being able to do extra pull-ups, remind me that progress comes through consistency. I am confident that the first business win is not far behind. With this freedom also comes the responsibility of self-directed accountability. I must design my own schedule and hold myself responsible for balancing personal, family, and professional priorities. My growth now comes through reading, podcasts, courses, and meetups. Attending the Financial Independence Meetup in Seattle reinforced that this path requires ongoing experimentation. I am exploring opportunities such as building a geographically diverse real estate portfolio, managing retirement accounts more directly, and considering ventures that combine financial expertise with helping others.

This season feels like more than a career break; it is an exploration of identity and purpose. Having spent many years on one path, I am learning adaptability in new ways. At the retirement party of my high school choir teacher, I reflected on the impact of his lifelong commitment to students. My legacy may look different, but the lessons of education continue to guide me. I hope to shape my new legacy through what I teach my children and by modeling economic self-sufficiency. I see the possibility of creating income streams that support my family for generations while helping my children grow in independence and resilience. As I walk around my new hometown, I notice how small businesses are interconnected and consider how I might contribute to the community in my own way.

Looking ahead, I carry forward the adaptability, curiosity, and careful planning gained from my career, travels, and financial work. Last year was a year of traveling Latin America. This year is a year of exploring entrepreneurship and investment opportunities. In five to ten years, or even next year, I may miss working with students and return to schools, or I may continue to pursue this new path. Either way, the choices I make now will provide valuable experiences and opportunities for my family. For me, success will be measured not only by financial growth but also by freedom, purpose, and meaningful connections. I look forward to this season of exploration and the chance to shape a life guided by my own choices.

Subscribe for Updates